UracilNitSecondTANDARD11624[Volt6 ]Demonstrate and use cognition of fiscal analysis

PerformanceDescriptionScope

Standards

|

Component 1 |

Explain the aims and restrictions of analysis of fiscal statements. |

1.1 The account identifies three users of fiscal and accounting statements and depict their aims for fiscal analysis.

1.2 The account identifies three

restrictions of fiscal analysis in footings of the procedure and the consequences of fiscal analysis.

|

Component 2 |

Calculate ratios to mensurate profitableness, plus use, working capital direction, long-run fiscal stableness, and fiscal markets. |

ratios – three ratios for profitableness, two ratios for plus use, two ratios for working capital direction, two ratios for long-run fiscal stableness, two ratios for fiscal markets. |

|

2.1 |

The selected ratios and sums are fit for intent. |

|

|

2.2 |

The computations are right and expressed in right units. |

|

|

Component 3 |

Report to direction on the consequences of fiscal analysis. |

|

|

3.1 |

The study is in a format appropriate for direction. |

|

|

3.2 |

The study compares and interprets ratios calculated for at least two accounting periods. |

ratios – profitableness, plus use, working capital direction, long-run fiscal stableness, solvency. |

|

3.3 |

The study includes comparing with another concern or industry benchmark. |

|

|

3.4 |

The study makes recommendations. |

|

|

3.5 |

Variations in the study content for a different terminal user are explained. |

terminal users must include one of – banker, investor, creditor, employee. |

|

Component 4 |

Demonstrate and use cognition of the solvency trial. |

4.1 Solvency trial is explained in

conformity with the Companies Act 1993 and its subsequent amendments.

4.2 Sums are selected and applied in conformity with the solvency trial, and a decision is drawn.

UracilNitSecondTANDARD9685[Volt6 ]Write an analytical study

|

LO |

Description |

Scope |

|

ER1 |

Plan the analytical study. |

|

|

1.1 |

The intent, audience and range of the study are determined and documented. |

|

|

1.2 |

Information is selected, analysed, and organised into a construction that fits the intent of the study. |

|

|

ER2 |

Write the analytical study. |

|

|

2.1 |

Report is consistent with the intent and organizational demands. |

Range – study may include but is non limited to – executive sum-up, abstract, footings of mention, debut, treatment, findings, decisions, recommendations, glossary, mentions, appendices ; grounds of at least five is required. |

|

2.2 |

The linguistic communication throughout the study is appropriate for the audience. |

Range – linguistic communication includes – spelling, punctuation, tone, vocabulary, grammar, sentence structure. |

|

2.3 |

Findingss are presented in a format that matches the information and the audience. |

Range – presentation may include but is non limited to – tabular arraies, graphs, text, diagrams. |

|

2.4 |

Report is written without prejudice. |

|

|

2.5 |

Decisions and/or illations drawn are consistent with findings. |

|

|

2.6 |

Any recommendations made are consistent with the intent, range, findings, and decisions. |

|

|

2.7 |

Report format is in conformity with the intent and organizational demands. |

|

|

ER3 Evaluate the effectivity of the analytical study. |

||

3.1 Audience feedback on the study is sought and

used to place any possible polishs for future studies.

RoentgenEPORTPhosphorusArtA:SecondUMMARYCHartRoentgenATIO ANDPhosphorusERCENTAGECALCULATIONS

BacillusACKGROUND

Briscoe Construction ( BC ) owns 3 big mills in New Zealand and a figure of edifice companies. It utilises a assortment of building techniques and is recognised as a specializer in its countries of expertness, all elements of building.

During the last twelvemonth BC has had diminishing hard currency flow and an increasing loss. They have identified that a good thought would be to sell off one of its edifice companies so they can beef up their overall trade name and fiscal stableness.

Two edifice companies that are potentially for sale are:

- Alpine Constructions Ltd.

- Maple Builders Ltd.

Alpine Constructions Ltd. is based in Masterton while Maple Builders Ltd. is based in Christchurch.

BC has been able to provide the undermentioned information about these companies. They would wish you to analyze the fiscal information supplied and complete the affiliated drumhead chart. Later in Part B you will be required to compose a study for them.

ASSIGNMENTRoentgenEQUIREMENTS

You are required to fix the undermentioned information and studies.

Ratio and Percentage Calculations

- Calculate appropriate ratios and per centums for both companies.

- Write your replies on the affiliated sheets.

- Your replies need to be typed into the Word papers “Assignment Ratio and Percentage Calculation Forms” which has been emailed to you ( you may utilize an suitably formatted Excel file if you wish ) .

- Separate A satisfies Unit 11624 PC’s 2.1, 2.2

- This assignments is to be submitted electronically via www.abacusinstitute.ac.nz/moodle by 5 PM on the due day of the month as above

OR

Alternate agreements can be made for presenting and subjecting your work with aid of the class instructor/tutor, in instance of any particular demands.

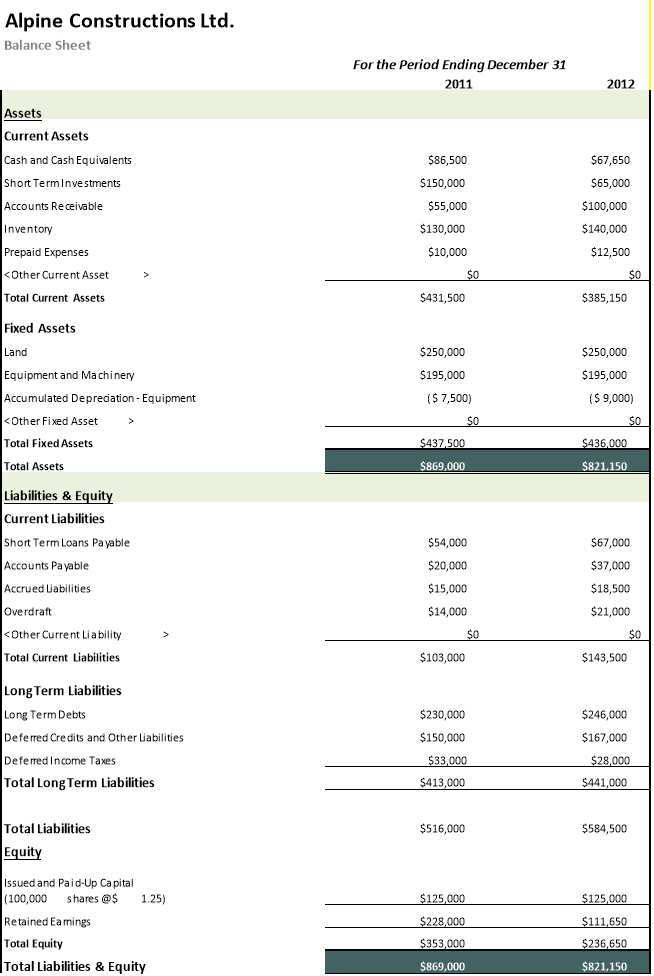

Alpine Constructions Ltd.

Income Statements

Year stoping 2011Year stoping 2012

Year stoping 2011Year stoping 2012

Gross saless

Cash Gross saless $ 160,000 $ 190,000 Credit Gross saless $ 1,550,000 $ 1,765,000

lessCog

Opening Inventory $ 97,000 $ 117,000

Direct labour $ 250,000 $ 500,000

Purchases $ 220,000 $ 320,000 Import Duties $ 15,000 $ 45,000

Freight in $ 22,000 $ 28,000

$ 604,000 $ 1,010,000

lessClosing Inventory$ 130,000 $ 140,000

Actual COGS Gross Net income

addOther Operating Gross

Dividends from Plumbers Direct $ 10,000 $ 12,000

Interest received $ 5,000 $ 7,000

$ 15,000 $ 19,000

Entire Gross Net income

LessOperating Expenses

Selling and Distribution

Advertising $ 90,000 $ 105,000 Freight out $ 70,000 $ 80,000

Gross saless wages $ 150,000 $ 165,000

$ 310,000 $ 350,000

General and Administrative

Rent $ 130,000 $ 145,000

Office wages $ 55,000 $ 60,000

Directors fees $ 50,000 $ 55,000

General Wages $ 80,000 $ 95,000

Depreciation on equip $ 10,000 $ 8,000

Power $ 15,000 $ 18,000

$ 340,000 $ 381,000

Finance

Interest on Overdraft $ 3,500 $ 6,500 Interest on 20 twelvemonth loan $ 50,000 $ 47,000

Bad debts $ 7,500 $ 10,000

$ 61,000 $ 63,500

Entire Operating Exp.

Net Net income ( T.G.P. – O.E. )lessIncome Tax Internet Net income After TaxlessDividends Paid

Retained Net incomes

Maple Builders Ltd.

Income Statements

Year stoping 2011Year stoping 2012

Year stoping 2011Year stoping 2012

Gross saless

Cash Gross saless $ 80,000 $ 110,000

Recognition Gross saless $ 1,215,000 $ 1,150,000

lessCog

Opening Inventory $ 65,000 $ 98,000 Direct labour $ 200,000 $ 285,000

Purchases $ 180,000 $ 210,000 Import Duties $ 12,500 $ 18,900

Freight in $ 22,000 $ 29,100

$ 479,500 $ 641,000

lessClosing Inventory$ 98,000 $ 140,000

Actual COGS Gross Net income

addOther Operating Gross

Dividends from Pumpkin Ltd. $ 7,800 $ 6,500

Interest received $ 3,500 $ 3,200

$ 11,300 $ 9,700

Entire Gross Net income

LessOperating Expenses

Selling and Distribution

Advertising $ 48,500 $ 44,500

Freight out $ 36,000 $ 28,000

Gross saless wages $ 85,000 $ 85,000

$ 169,500 $ 157,500

General and Administrative

Rent $ 55,000 $ 57,000

Office wages $ 25,000 $ 29,000

Directors fees $ 45,000 $ 45,000

General Wages $ 65,000 $ 75,000

Depreciation on equip $ 7,500 $ 6,500

Power $ 11,000 $ 15,000

$ 208,500 $ 227,500

Finance

Interest on Overdraft $ 6,500 $ 7,000 Interest on 20 twelvemonth loan $ 25,000 $ 25,000

Bad debts $ 8,000 $ 10,000

$ 39,500 $ 42,000

Entire Operating Exp.

Net Net income ( T.G.P. – O.E. )lessIncome Tax Internet Net income After TaxlessDividends Paid

Retained Net incomes

Maple Builders Ltd.

Balance Sheet

For the Period Ending December 31

20112012

|

Assetss |

||

|

Current Assetss Cash and Cash Equivalents Short Term Investments Histories Receivable Inventory Prepaid Expenses & lt ; Other Current Asset & gt ; Entire Current Assets Fixed Assetss Land Equipment and Machinery Accumulated Depreciation – Equipment & lt ; Other Fixed Asset & gt ; Entire Fixed Assetss |

$ 135,000 $ 130,000 $ 36,500 $ 98,000 $ 12,000 $ 0 |

$ 26,500 $ 128,000 $ 50,000 $ 140,000 $ 12,500 $ 0 |

|

$ 411,500 $ 280,000 $ 125,000 ( $ 5,500 ) $ 0 |

$ 357,000 $ 280,000 $ 240,000 ( $ 21,500 ) $ 0 |

|

|

$ 399,500 |

$ 498,500 |

|

|

Entire Assetss |

$ 811,000 |

$ 855,500 |

|

Liabilities & A ; Equity |

||

|

Current Liabilitiess Short Term Loans Collectible Histories Collectible Accrued Liabilitiess Overdraft & lt ; Other Current Liability & gt ; Entire Current Liabilitiess Long Term Liabilities Long Term Debts Deferred Creditss and Other Liabilitiess Deferred Income Taxes Entire Long Term Liabilities Entire LiabilitiessEquity Issued and Paid-Up Capital ( 100,000 portions @ 1.50 ) Retained Net incomes Entire Equity |

$ 45,000 $ 22,000 $ 21,000 $ 8,000 $ 0 |

$ 68,500 $ 45,000 $ 20,000 $ 16,500 $ 0 |

|

$ 96,000 $ 190,000 $ 89,000 $ 21,000 |

$ 150,000 $ 226,000 $ 115,000 $ 26,500 |

|

|

$ 300,000 |

$ 367,500 |

|

|

$ 396,000 $ 150,000 |

$ 517,500 $ 150,000 |

|

|

$ 265,000 |

$ 188,000 |

|

|

$ 415,000 |

$ 338,000 |

|

|

Entire Liabilities & A ; Equity |

$ 811,000 |

$ 855,500 |

Part A: Drumhead Chart Ratio and Percentage Calculations

|

Alpine Construction Ltd. |

Maple Builders Ltd. |

|||

|

2011 |

2012 |

2011 |

2012 |

|

|

Solvency Ratios |

||||

|

Profitability Ratios |

||||

|

Asset Utilization Ratio |

||||

|

Fiscal Market Ratio |

||||

|

Long Term Financial Ratio |

||||

|

Working Capital Ratios |

||||

Market indexs for the Building Industry:

|

Measure |

Industry criterion |

|

Gross Net income % |

60 % |

|

Net Net income % |

20 % |

|

Rate of Return on Assetss |

33 % |

|

Cog |

30 % |

|

Current Ratio |

2:1 |

|

Equity Ratio |

60:40 |

|

Inventory Employee turnover |

6.2 times |

|

Histories Receivable ( yearss ) |

43 yearss |

|

EPS |

$ 1.28 |

|

Pe |

3.30 |

RoentgenEPORTPhosphorusArtBacillus:RoentgenEPORT ONPhosphorusROFIT,SecondTABILITY ANDTocopherolFFICIENCY

BacillusACKGROUND

Briscoe Construction ( BC ) has been able to obtain information about these companies. They would wish you to fix a study that includes advice to them on ( study subdivision Numberss provided ) :

Note: Your study should be structured in a format detailed on the following page, and your analysis/findings/discussion subdivision must cover the undermentioned:

- Which subordinate provides the best long term net income potency (Profitableness) ;

( 11624 Personal computers 2.1, 2.2, 9685 ERs 1.1, 1.2, 2.3 )

- Which subordinate is in the most financially stable place (FINANCIAL STABILITYANDWORKING CAPITAL MANAGEMENT) ;

( 11624 Personal computers 2.1, 2.2, 9685 ERs 1.1, 1.2, 2.3 )

- Which subordinate is run most expeditiously (ASSET UTILISATION) ?

( 11624 Personal computers 2.1, 2.2, 9685 ERs 1.1, 1.2, 2.3 )

- Which subordinate is in the best market place (FINANCIAL MARKETS) ?

( 11624 ERs 2.1, 2.2, 9865 ERs 1.1, 1.2, 2.3 )

- Which subordinate is the most solvent? (Solvency) ?

( 11624 Personal computers 2.1, 2.2, 4.1, 4.2, 9685 ERs 1.1, 1.2, 2.3 )

- Which subordinate compares most favorably within the industry( Industry) ?

( 11624 Personal computers 2.1, 2.2, 3.3, 9685 ERs 1.1, 1.2, 2.3 )

- State which company BC should deprive. You must supply grounds for your recommendation.( Note divest the best overall executing administration )

( 11624 Personal computer 3.4, 9685 ERs ERs 1.1, 1.2, 2.3, 2.5, 2.6 )

i‚· Detail anybettermentsto be made or actions taken after the divesting of the subordinate( Internet Explorer: to the staying subordinate that you don’t sell ) .

( 11624 Personal computer 3.4, 9685 ERs 1.1, 1.2, 2.3, 2.5, 2.6 )

- State at least three ( 3 )restrictionsandfluctuationsthat might be to your analysis. These must be specific to the terminal user. Besides remark must be included as to how the study would change if presented to a bank.

( 11624 Personal computers 1.2, 3.5 )

- Seek audience feedback on your study( mention Student Feedback Report ), and utilizing this feedback place any possible polishs for future studies.

( 9685 ER 3.1 )

Report Structure and content ( 10-15 pages about, 1500-2500 words about )

Executive Summary( 1 page, 300 words ) ( to summarize the full study including Introduction ( intent ) , Methodology, Results, and Recommendation )

1.0Introduction: ( 1 page )

The debut should incorporate the followers:

- State the background ( purpose ) to this study,

- Overview the fiscal analysis constructs used in fixing this study,

- Identify the demands of possible users ( range ) of this study ( minimal of 3 identified ) and ;

- Overview the contents of this study

2.0Analysis/Findings( 5-7 pages )

Analysis: What do the consequences tell us?

Findingss: What did you happen? State the reader utilizing formats such as graphs tabular arraies etc

Example for a subdivision: Profitableness, Asset Utilisation etc

Profitableness: Justify your reply to the inquiry“Which company provides the best long term net income potency? ”You must straight and specifically reply the inquiry, giving grounds for your reply. In warranting your reply to the inquiry, use the ratios and per centums calculated as thegroundsfor ( and to assist place ) any issues.

3.0Discussion: ( 2-3 pages )

Based on your analysis/findings above, discourse the fiscal health/position of each company.

4.0Decision: ( 1 page )

Should pull on your analysis/findings above.

5.0Recommendations: ( 1/2 page )

Based on your analysis above,do a recommendationon which company BC Limited should deprive. First you mustexplicate the groundsfor doing this recommendation. You must deprive the strongest acting concern.Note: In this study your recommendation and decision are efficaciously combined

6.0Recommended Improvements:( 1/2 – 1 page )

Suggestthreeways of bettering the concern you haverecommendedfor non depriving. These suggestions should be practical, specific and explained in sensible item. Each suggestion must be clearly different from the others. They must non all relate to the same issue or facet of the concern.

7.0Restrictions: (1/2 page )

Suggest possible restrictions of the fiscal analysis including: signifier and content, accounting measuring, categorization, materiality, consistence, comparison, and neutrality.

8.0Reference List: ( if used )

9.0Appendixs: Any extra information that needs to be supplied to the reader. (non included in word bound )

( 11624 Personal computer 1.1, 9865 ERs 1.1, 1.2, 2.1, 2.5, 2.6, 2.7 )

10.0The study must besides:

- Be conducted over two accounting periods ( 11624 Personal computer 3.2 )

- Be conducted for both entities as possible parts of BC’s concern operations under the headers provided ( 11624 Personal computer 3.2 )

- Have clearly determined and documented intent, audience and range ( 9685 ER 1.1 )

- Have information that is selected, analysed and organised into a structured that fits the intent of the study, be consistent with organizational demands and audience, and be written without any prejudice ( 9685 ERs 1.2, 2.1, 2.4, 2.7 )

- Be written throughout in linguistic communication ( inc. spelling, punctuation, tone, vocabulary, grammar and sentence structure ) such that it is appropriate for the audience ( 9685 ER 2.2 )

- Present findings in a format ( e.g. , tabular arraies, graphs, text, diagrams, other ) such that your presentation/interpretation matches the information and the audience ( 9685 ER 2.3 )

- Ensure that decisions and/or illations you have drawn from analysis are consistent with findings ( 9685 ER 2.5 )

- Propose recommendations in a mode that these are consistent with the intent, range, findings and decisions ( 9685 ER 2.6 )

- Demonstrate that audience feedback has been sought by you and used to place any possible polishs for future studies ( 9685 ER 3.1 )

They have set aside the Board meeting in late May to discourse this, so I need your study completed and delivered to them by the due day of the months as outlined. This will give me clip to direct it to all Directors for their consideration. BC’s Board of Directors will do the concluding determination as to which company to deprive, but the determination will trust to a great extent on your study.

SecondTUDENTFEEDBACKRoentgenEPORT

SecondTUDENTNitrogenAME:______________________________

UracilNitSecondTANDARD11624[Volt6 ]Demonstrate and use cognition of fiscal analysis

|

Performance Standards |

Remark |

Achieved |

Not Achieved |

|

1.1 |

|||

|

1.2 |

|||

|

2.1 |

|||

|

2.2 |

|||

|

3.1 |

|||

|

3.2 |

|||

|

3.3 |

|||

|

3.4 |

|||

|

3.5 |

|||

|

4.1 |

|||

|

4.2 |

|||

|

5.1 |

|||

|

5.2 |

|||

|

5.3 |

|||

|

5.4 |

|||

|

5.1 |

SecondTUDENTFEEDBACKRoentgenEPORT

SecondTUDENTNitrogenAME:______________________________

UracilNitSecondTANDARD9685[Volt6 ]Write an analytical study

|

Erbium |

Remark |

Achieved |

Not Achieved |

|

1.1 |

|||

|

1.2 |

|||

|

2.1 |

|||

|

2.2 |

|||

|

2.3 |

|||

|

2.4 |

|||

|

2.5 |

|||

|

2.6 |

|||

|

2.7 |

|||

|

3.1 |

( 9685 ER 3.1 )

National Diploma in Business Level 51 Assignment Parts A & A ; B, Accounting & A ; Fin Man 2014